The dollar supremacy

Money is memory, as the economist Narayana Kocherlakota once wrote. Ultimately, the dollars in a person’s wallet, or checking account, are a record of having produced something of value to someone else, an entry in a cosmic ledger.

- But memories can be forgotten. The Russian government and countless Russian companies and individuals are learning that the hard way.

Why it matters: Within the space of just a few days, the U.S. and its allies accomplished the astonishing feat of cutting Russia out of the global financial system. In the process they may have further entrenched the centrality of the U.S. dollar to the global economy.

The big picture: The Russian government had built up $630 billion in reserves to protect its economy against capital outflows. It now looks largely useless after the U.S. and allies cut off the Russian central bank’s access to West.

- In a way, it’s a startling reminder of the sheer power that nation-states have over the use of currency. In just a few days, they turned the world’s 11th largest economy into the equivalent of a drug kingpin sitting on a big pile of un-laundered cash they can’t spend.

Traditionally, there has been a tradeoff when the U.S. takes advantage of the dollar’s primacy in the world economy to implement its foreign policy goals. The more that power is used, the more you risk losing it.

- So when the U.S. has enforced sanctions on Iran, North Korea and other countries by threatening those who violate them with cutting off access to the dollar-based financial system, it increases the urgency of China and other nations to create international financial alternatives.

In its scale and speed, the retaliation against Russia dwarfs any previous use of the global banking system to cut a nation out and render its assets unusable. So an important question is whether it commensurately puts the whole thing at risk.

Yes, but: This is not a situation in which the U.S. is acting alone. Rather, it is represents a rare moment of global unity, in which the vast majority of nations are appalled by Russia’s actions, as evidenced the U.N. General Assembly vote to condemn the invasion: 141 to 5 with 35 abstentions.

- In that sense, it amounts to a moment when the value of the dollar-based global financial system is in clearer view — it creates a mechanism for the world to come together and call out a bad actor.

- As Bloomberg’s Matt Levine puts it, “If you do something so outrageous that society as a whole decides you are a pariah, then money is a way for society to express that.”

The bottom line: Yes, there is always risk that using the tools of financial warfare will make them less useful in the future. But Russia’s invasion is also showing the world just how costly it is to become a pariah state.

Go deeper: The dollar remains the West’s ace in the hole

– That ’70s show

It can be risky to draw too many historical parallels when analyzing the economy. Whatever the similarities between the current economic moment and any past episode, they’re usually dwarfed by the differences.

- Still, the surge of commodity prices that has accompanied the Russian invasion of Ukraine makes for a striking parallel between the 2020s and the 1970s.

Why it matters: The conflict in Eastern Europe risks affecting the economy in similar ways as the oil embargo of five decades ago. That implies bringing inflation down will be a slower and more painful process than policymakers have been counting on.

Flashback: Inflationary pressures were building through the late 1960s and early 1970s, fueled by high government spending and rapidly rising wages. Then in 1973, the U.S. role in the Arab-Israeli war prompted OPEC to embargo the U.S. from its oil exports. That sent oil prices skyrocketing.

- That’s the kind of price shock that central banks can’t do anything about. But coming as it did at a moment of already-elevated inflationary psychology, it helped cause expectations of ever-rising prices to become more entrenched

- Moreover, it heightened generalized discontent with the economy, the sense that things were coming unmoored beyond the details of any given piece of inflation data.

The parallels: Now, too, inflation is already high, in part due to government spending rising wages. And the war in Ukraine is causing commodity prices to soar.

- The risk is that, as in 1973, external geopolitical events reinforce pre-existing trends in the domestic economy, while simultaneously making it politically harder for policymakers to fight inflation.

Yes, but: That’s not how Fed chair Jerome Powell views it. Asked whether the 1970s are an apt historical comparison in a congressional hearing this week, he said, “That’s the proper historical reference for what we’re trying not to replicate.” (Emphasis mine.)

- One difference between now and then: Central bankers’ conviction that it’s their job to bring inflation down to an explicit target, Powell said.

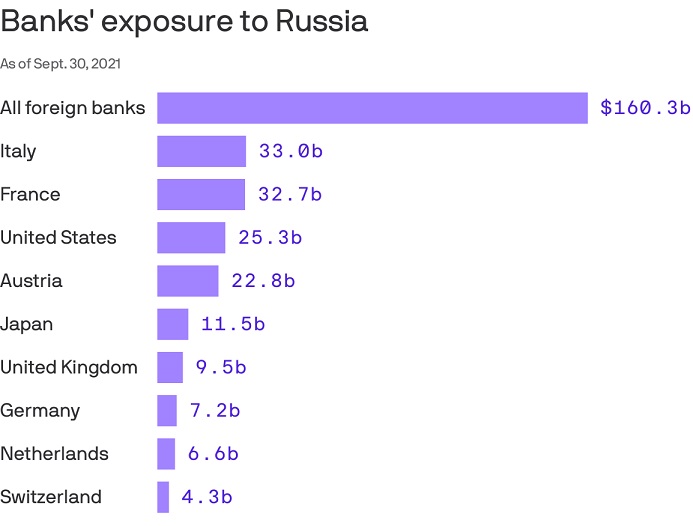

– Banks’ Russia exposure

Source: Bank for International Settlements using calculation method from The Overshoot; Chart: Axios Visuals

Western banks have seriously cut back on their exposure to Russia since the 2014 Crimea invasion. But that doesn’t mean they aren’t exposed to substantial losses as the nation is cut off from the global financial system.

By the numbers: Foreign banks had about $111 billion in immediate exposure to Russia at the end of September, and another $49 billion in indirect exposure like derivatives contracts and credit guarantees. That’s down from a combined $450 billion in 2013.

- Those numbers are from Bank for International Settlements data as crunched by Matthew Klein in his newsletter, The Overshoot, who uses a method aimed at summarizing banks’ total financial exposure.

French and Italian banks have the most direct exposure, followed closely by Austria — though Austrian banks’ exposure is much higher relative to the size of its economy.

The American banking system has trivial exposure to Russia relative to its size: $25 billion total, in a $22.6 trillion banking system.

Πηγή: axios.com